- Accurate, licensed deed and mortgage data underpins every reliable title search, helping insurers spot defects, liens, and fraud before a policy is issued.

- Nearly 30% of title insurer losses come from problems that a basic public-records search cannot uncover, which is why validated, multi-source data matters so much.

- Bulk data licensing gives insurers centralized, standardized access to deed and mortgage records, cutting manual retrieval errors and speeding up underwriting.

- AI-driven analytics and blockchain are set to reshape how the industry verifies ownership and prices risk over the next few years.

Title insurance companies work in a high-stakes environment. Their financial stability rests on one thing above all, and that is accurate property data. When a record is wrong, missing, or fraudulent, the insurer absorbs the loss. So the quality of deed and mortgage data is not a back-office detail. It is the core of the business.

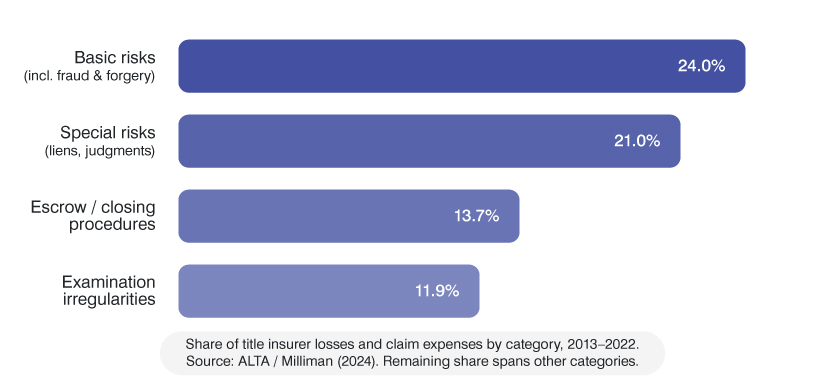

The numbers make the point. Between 2013 and 2022, U.S. title insurers paid roughly $4.4 billion in claims and loss expenses, according to an independent analysis by the actuarial firm Milliman, commissioned by the American Land Title Association (ALTA).

Nearly 30% of those losses traced back to title problems that a standard public-records search could not catch, including fraud, forgery, and escrow errors. Fraud and forgery alone made up 21% of claim dollars, at an average cost of more than $143,000 per claim, against roughly $26,000 for all other claim types.

That gap, between what public records show and what is actually true about a property, is exactly where reliable deed and mortgage data earns its value. Mortgage data providers supply property data solutions for deed verification and mortgage title searches that help close it. The rest of this article walks through how that data works, why licensing it matters, and where the industry is heading.

Table of Contents

- Understanding licensed deed and mortgage data

- Why licensed deed and mortgage data is critical for title insurance

- How deed and mortgage data supports title insurance companies

- Deed records vs. mortgage records and what each one tells you

- Leveraging bulk data licensing solutions for title insurance

- Case study: AI-powered title search automation for a title insurer

- Future trends in deed and mortgage data usage

- Frequently asked questions

- Conclusion

Understanding licensed deed and mortgage data

Licensed deed and mortgage data is the foundation of a sound title search. It lets insurers verify real estate records, assess risk, and issue accurate policies. The data reveals a property’s ownership history, its financial obligations, and any legal encumbrances that could derail a transaction.

Two record types do most of the work. A deed record establishes the chain of title. A mortgage record establishes the financial claims against the property. Each carries a distinct set of fields.

- Deed records include grantor and grantee names, the legal property description, the transfer date, and the consideration amount.

- Mortgage loan data includes the lender, loan amount, interest rate, and terms, which form the basis for any mortgage lien search.

- Public mortgage data surfaces outstanding liens or encumbrances that could cloud ownership.

Insurers pull this data from several places, and each source has its own strengths and gaps.

- County recorder’s offices, courthouses, and land registries, which form the primary public record.

- Title plants, the private, geographically indexed databases that title companies maintain to speed up searches.

- Mortgage data providers, who aggregate and standardize records across jurisdictions.

But availability is not the same as accuracy. A record can exist and still be wrong. Errors in real estate data lead directly to title defects, ownership disputes, and fraudulent claims. To guard against that, insurers run rigorous validation that includes cross-verification across multiple sources, AI-driven error detection, and automated quality-control checks.

In our own work indexing county records for title-plant clients, the single most common issue we encounter is not a missing document. It is a prior mortgage that was satisfied in practice but never marked as discharged in the public index. That one gap, left unresolved, is enough to stall a closing.

Why licensed deed and mortgage data is critical for title insurance

Licensed data is the bedrock of title insurance because property transactions are unforgiving of error. These datasets are not just records. They are the insurer’s primary tool for managing risk.

Comprehensive data lets insurers run an exhaustive title search and establish a clean chain of title. Without it, hidden encumbrances, undisclosed heirs, or fraudulent activity can slip through, and the insurer pays for what it missed.

Mortgage loan data adds a second layer, showing the financial claims against a property so the insurer can gauge foreclosure risk and reflect the true status in the policy. This accuracy also supports the disclosures lenders must give borrowers at closing, which the Consumer Financial Protection Bureau oversees.

Licensing matters for a third reason, which is integrity. Records from reputable, licensed providers have already been through validation, which lowers the odds of acting on a forged document or a stale entry. Given that fraud and forgery claims rose from 19% of basic-risk claims in 2013–2020 to 44% in 2022 alone, that pre-validation is no longer a nicety. It is a defense against a fast-growing threat.

How deed and mortgage data supports title insurance companies

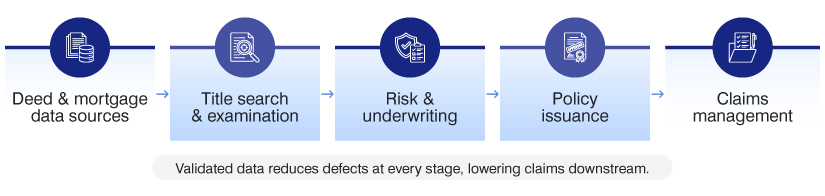

Deed and mortgage data shows up at three points in the title insurance workflow, which are the search, the underwriting decision, and any claim that follows. The diagram below traces how data moves through that process.

The key ways deed and mortgage data supports title insurance companies are described below.

Strengthens title searches and examinations

Before issuing a policy, insurers run title searches to verify ownership and surface risk. Deed transfer data and public mortgage data reveal a property’s history and help catch defects before closing.

Specifically, this data confirms three things:

- Deed records confirm grantor and grantee names, the legal description, and ownership history.

- Mortgage loan data confirms lender details, loan amounts, interest rates, and terms.

- Mortgage title searches flag outstanding liens or encumbrances that affect ownership rights.

Incomplete or outdated records cause ownership conflicts and raise the odds of a claim. Advanced providers solve this by aggregating records from county recorders and title plants, then running automated validation to flag anomalies. The result is a defensible search rather than a hopeful one. Comprehensive deed verification lets insurers fix problems before they become claims.

Enhances risk assessment and underwriting

Deed and mortgage data drives the underwriting decision. By analyzing the record, insurers gauge the odds of ownership conflicts, boundary disputes, or fraudulent sales.

The data helps in three concrete ways:

- Deed verification confirms past transfers, prior claims, and boundary disputes.

- Historical mortgage records flag red flags such as repeated rapid transfers.

- Mortgage lien searches reveal unpaid loans, tax liens, or conflicting claims.

Consider a common case. A property carries two mortgages recorded years apart. Public mortgage data lets the underwriter check whether the first loan was properly discharged. If the release was never recorded, the insurer knows to resolve it before issuing the policy, not after a claim lands.

AI-powered title production workflows now handle this matching across large volumes, which cuts manual error and tightens underwriting accuracy. Cleaner inputs let insurers price coverage to the property’s real risk profile.

Simplify Title Searches with Bulk Data Licensing

Gain instant access to deed and mortgage records for accurate underwriting.

Supports claims management and resolution

When a claim arises, deed and mortgage data becomes the evidence. Accurate public mortgage data lets insurers pin down the cause of a defect and assign liability.

The data supports resolution in three ways:

- Deed records provide legal proof of ownership for the investigation.

- Mortgage data verification shows whether unpaid debts, tax liens, or fraud drove the dispute.

- Historical loan data traces undocumented transactions or improperly discharged mortgages.

Resolving a claim usually means retracing a property’s ownership history to confirm whether a deed transfer or lien release was handled correctly. Without complete records, that work is slow and costly.

Mortgage data providers supply the historical view of payments, refinances, and foreclosure records that lets insurers settle disputes quickly. Given that fraud and forgery claims are among the three costliest causes of loss, fast, data-backed resolution directly protects the bottom line.

The chart below shows where title insurer losses actually come from, based on the ALTA and Milliman analysis of claims from 2013 to 2022. Basic risks, which include fraud and forgery, top the list, and most of these problems cannot be found through a routine public-records search.

Deed records vs. mortgage records and what each one tells you

Deed records and mortgage records answer different questions. The first establishes who owns the property; the second establishes what is owed against it. A complete title picture needs both.

| Attribute | Deed record | Mortgage record |

|---|---|---|

| Primary purpose | Establishes ownership and chain of title | Establishes financial claims against the property |

| Key parties | Grantor and grantee | Borrower and lender |

| Core fields | Legal description, transfer date, consideration amount | Loan amount, interest rate, terms, maturity |

| Main risk it surfaces | Undisclosed heirs, forged transfers, boundary disputes | Unpaid liens, undischarged loans, foreclosure exposure |

| Used most in | Title search & ownership verification | Lien search & risk assessment |

Leveraging bulk data licensing solutions for title insurance

Bulk data licensing gives insurers centralized access to deed and mortgage records, which makes searches, risk assessment, and claims work faster and more consistent. Instead of pulling fragmented records source by source, insurers license standardized datasets from providers, county recorders, and title plants, then work from one reliable view.

The practical gains are concrete. Centralized datasets let insurers identify ownership history, encumbrances, and outstanding mortgage obligations quickly, with fewer manual-retrieval errors. That speeds underwriting and sharpens policy issuance.

Layer AI-driven risk analysis on top, and insurers can flag fraudulent transactions and inconsistent ownership transfers that a manual review might miss. The payoff is lower claims costs and steadier financial footing.

This upfront prevention is why the industry runs such a low loss ratio, which the National Association of Insurance Commissioners put at 5.1% for the U.S. title sector at the end of 2024, far below most other insurance lines.

Enhance Risk Assessment with Mortgage Data Verification

Identify title defects, prevent fraud, and improve underwriting with accurate data.

How AI-Powered Title Search Automation Cut Turnaround Time for a Title Insurer

The value of clean, well-sourced data is easiest to see in a live operation. One of the top four title insurance underwriters in the United States faced a familiar problem. Its supporting documents were scattered across multiple title plants and county record systems, and that fragmentation slowed retrieval and review.

At the same time, the underwriter had to meet strict turnaround windows of four to eight hours while holding to a 100% accuracy standard on ownership and lien data.

Working with Hitech i2i on title search production for properties in Georgia and Texas, the underwriter automated document ingestion and the extraction of key property, lien, assessment, and tax fields.

Low-confidence and critical fields were routed to human-in-the-loop validation, so automation handled volume while people guaranteed accuracy. The measurable results show what good data and workflow design deliver together.

- 30% increase in analyst productivity across title search operations.

- 85%+ automated extraction accuracy, backed by human validation to ensure 100% final accuracy.

- 8-hour orders delivered in under 5 hours, with similar gains across other title products.

The pattern mirrors the point made earlier about undischarged liens and scattered records. When data from many sources is consolidated, validated, and structured, the search gets both faster and more reliable. You can read the full title search automation case study for the complete workflow.

Future trends in deed and mortgage data usage

The direction of travel is toward more automation and tighter integration. Several shifts are already underway, as the points below describe.

- AI-driven analytics will refine risk assessment and predict title defects earlier. Document-extraction models already pull lien, tax, and ownership fields from scanned records at scale, leaving examiners to validate rather than re-key.

- Blockchain may improve data security and ownership transparency. Several U.S. county recorders have already piloted blockchain-based deed recording to create tamper-evident transfer histories.

- Real-time data updates will speed transaction processing and shrink the lag between a recording and a search.

- Cloud platforms and open APIs will let insurers, lenders, and real estate professionals share data and plug it directly into existing workflows.

- Data standardization will improve interoperability across jurisdictions and platforms.

Together, these trends point to a title insurance process that catches problems earlier and resolves them faster. The insurers that invest in clean, well-licensed data now will be best placed to use these tools as they mature.

Frequently asked questions

What is licensed deed and mortgage data?

It is property record data covering ownership transfers and loan obligations, sourced under license from providers, county recorders, or title plants. Licensing typically means the data has been aggregated, standardized, and validated, so insurers can rely on it for title searches and underwriting.

What is a title plant?

A title plant is a private, geographically indexed database of property records maintained by a title company or data provider. Because it is organized by property rather than by name or date, it lets examiners run a title search far faster than searching raw public records.

What causes most title insurance claims?

According to the ALTA/Milliman analysis of 2013–2022 claims, nearly 30% of title insurer losses came from problems undetectable in a basic public-records search, with fraud and forgery the costliest category at over $143,000 per claim on average.

How do title companies verify liens?

They run a mortgage lien search against public and licensed mortgage data to find outstanding loans, tax liens, and judgments, then confirm whether each has been properly discharged or released in the record.

Why does data accuracy matter so much in title insurance?

Because the insurer absorbs the cost of any defect it misses. A single unrecorded lien release or forged deed can trigger a claim that costs six figures, so validated, multi-source data is the most cost-effective form of risk control.

Conclusion

Licensed deed and mortgage data sits at the center of title insurance. It powers the title search, informs the underwriting decision, and provides the evidence that resolves claims. Bulk licensing makes that data faster to use and easier to trust, while AI and blockchain promise to sharpen both accuracy and speed in the years ahead.

The throughline is simple. The cleaner and better-validated the data, the fewer defects reach a policy, and the fewer claims follow. For title insurers, investing in high-quality property data is not overhead. It is the most direct path to protecting both their customers and their margins.

Enhance Risk Assessment with Mortgage Data Verification

Identify title defects, prevent fraud, and improve underwriting with accurate data!